No matter how many clever and snarky op/eds he writes in the NY Times claiming that we can – and MUST -- fix the economy via money printing (and if you dare to disagree of course you are a sinister member of the anti-poor 1%), Paul Krugman can’t change the basic laws of nature that determine what is and is not possible in the economy.

There is for example, the law of no free lunches which specifies that a central bank CANNOT inject prosperity – nor can it inject income inequality or sustainability or new technology or wealth or health -- into the economy or society by printing money out of thin air. When money printing inevitably fails, the money printing advocates (like Krugman) have one of two arguments at their disposal: they either callim that the central bank didn’t do enough – as with Japan. Or, they claim central bank did too much (Weimer Republic) and of course they'd never make that mistake.

THese experts claim this despite the fact that never, ever in the history of the world has a country successfully produced a durable and sustainable period of robust economic growth with peace and social harmony via a historically unprecedented central bank money printing operation. NEVER.

money printing correlates to war (WWI, Vietnam, Iraq) which then inevitably leads to economic and financial bubbles as we saw Roaring 20s come direclty after WWI; and the Great inflation of 1970s after Vietnam; and finally the great global asset and real estate bubble following the War on Terror. Each boom of course was followed by a bust, the Great Depression, the 198101983 Recession, and now the 2008-9 global credit crunch and Recession that has yet to fully play out. although the Fed promises everything will turn out just fine...

The Bernanke view of the Great Depression claims that the Fed failed the economy and caused the Great Depression by not printing enough money after the Great Crash of 1929. We are supposed to believe that if the Fed had just done more money printing in the 1930s everything would have turned out okay aside from dealing with the effects of the initial stock market crash.

How do we know this for sure? How do we know how the economy and financial sector would have evolved if the Fed had in fact printed enough money? Could the Fed have prevented the Great Depression?

This is exactly the “experiment” we are running now!!! The Fed created a massive global credit and asset bubble in the 2000s thanks to easy money policy that led to the 2008 credit crunch and 2009 global recession. "Luckily" for all of us, the Great Ben Bernanke has been pulling the monetary levers at the Fed so he could implement the lessons learned from the Fed’s failure in the 1930s to prevent the Great Depression. We have been told that the Fed bailed us out in 2008-9 with money printing, and if we want to fix the economy for good, we just need some more money printing to finish the job.

"We" believe this despite the fact that no central bank has ever successfully “fixed” an economy via sustained money printing. Money printing is what causes economic booms and busts in the first place. If you look at sustained periods of dynamic (but not extraordinary) growth and wealth creation and peace (or no major war), these periods are correlated with relatively sound money regimes, such as the period from 1950 to 1965 and from 1983 to 1996. War, booms, bubbles, stagflation and inevitably ... busts ... these are all correlated to periods of easy money. the Fed was established in 1913. the Fed cranked up printing press to help pay for US entry into WWI. the roaring 20s was facilitated by Fed policy aimed at surpressing interest rates, the 1930s was a mess thanks to the post WWI and Roaring 20s easy money boom. the US economy remained depressed in the 1940s all through WWII which again was a period of currency debasement and easy money. Only when the Fed stopped the printing presses in the 1950s was the economy able to generate sustained growth and productivity gains. in the 1960s we cranked up the printing presses once again for the Vietnam War and for the great society experiment. That led directly to the Great inflation of the 1970s. We were told that central banks had it already figured out in the early 2000's and that global inflation had been defeated and that high and sustainable growth was at hand ... little did the powers to be suspect that building below what appeared to the experts as a health global economy was a massive easy money bubble -- accomodated and triggered by a combination of the modern fedish for inflation targeting and the easy money policy required to pay for the War on Terror.

The law of no free lunches specifies that no Central Bank can fix an economy by printing money. A corollary to the law of no free lunches is that when the Central bank does print money, it does so at the cost and NOT the benefit of the so called ‘poor.’ Money printing is non-neutral: it favors the politically connected who are the wealthiest in society. Money printing favors those who own assets, like real estate and stocks and like large financial firms, because this is where money printing goes first!!! those on fixed incomes, the poor who own few or in most cases no assets get screwed as their incomes are fixed – and yet prices go up. The Fed loves to use core CPI because it strips out food and energy prices and gives them more flexibility to engineer monetary policy without constraint, even though the poor must spend a much higher percentage of their disposable income compared to the so called “wealthy” on food and energy. Inflation also helps the government erase debt obligations. The government giveth (very loudly and boldly) to the so called poor BUT then the government taketh away (very secretly) via inflation and money printing. Meantime, when money printing creates new bubbles and distorts the economy and leads to poor economic performance, the government is quick to blame the market for screwing up again.

IF the government could just give to the so called poor without taking anything away from society, then what are we waiting for?

Paul Krugman has it exactly upside down: the Fed’s money printing will make the rich even richer and the poor even poorer. We are already seeing concentration in the financial industry INCREASE since 2008! Income inequality keeps going up, and will keep going up no matter how high we make marginal tax rates.

Who really believes in their heart of hearts that society may benefit if and when a central bank prints money as long as CPI (or core CPI) stays low? If that were really possible, well then the law of no free lunches would be proven wrong. We could pick money off of trees and give it to the most deserving in society without any trade off or problem or net cost to society. The idea that CPI measures “inflation” is a clever way for the Fed to pretend we can have our cake and eat it too.

America wake up! Money printing is not a free lunch no matter whether or not CPI or core CPI stays low and stable or not. Money printing is very expensive and we will pay the piper one way or the other with rising political and social tension, financial market volatility, lower productivity, higher structural unemployment, lower trend GDP growth, less liberty and eroded moral values. Easy money is a major source --if not “the” fundamental source -- of evil in society – it has been since Roman empire … and I fear there will always be politicians and experts to promise free lunches via new money printing technologies in the future.

If it sounds too good to be true, it usually is. Life isn’t fair. that is what we teach our children. Why don’t we expect our politicians to live by these words?

The Scourge Of Central Banking

Yesterday, Dylan Grice of Societe Generale published a brief piece on the debasement of money that has rightly garnered quite a bit of attention. Readers who have missed it can read a summary of the salient points at Zerohedge.

As we have mentioned in the past, Grice appears to be a 'closet Austrian'. He regularly advocates Austrian ideas and viewpoints, but we have never seen him identify them as such. Be that as it may, it is the ideas that count, not their label. It should perhaps also be pointed out in this context that people like Ludwig von Mises or Murray Rothbard did not see themselves as 'Austrian' economists either - rather they felt they were simply economists advancing the science of economics - albeit economists whose work was certainly firmly rooted in the subjectivist tradition of the Austrian school.

To return to Grice, he makes several important points that are well worth considering. For one thing he points out that the institution of money is extremely important to social cooperation. In order for the market economy to function, one must trust a great many people one doesn't know. Money is the means by which this trust is established: we can assign value to the goods and services offered to us by others in monetary terms. They in turn can do the same with thew things we offer them.

It follows that when money is debased, social cooperation is hampered. There is even more to this in fact: the fiat money system, which has become such an indispensable feature of the modern-day welfare-warfare State, severely erodes peoples moral values. This is because it enables the belief that one can get something for nothing to become ever more entrenched.

The 'spontaneous order' of the market economy depends on the ability of economic actors to calculate and to receive proper price signals. Sound money is thus an indispensable feature of a healthy market economy.

In 'normal times' we can be fairly certain that the value of money won't fluctuate around a lot. Peoples' expectations about the purchasing power of money today are informed by their knowledge of its purchasing power of yesterday, and so on, in an infinite regression. Of course money has no 'fixed value' - there are no constants in economics and money is no exception to this rule - but it should be obvious that it is extremely important that one be able to rely on money's ability to fulfill the functions outlined above. When the authorities begin to debase money in ever greater strides, this is soon no longer the case.

Grice uses a number of historical case studies to drive the point home: once the debasement of money crosses a certain threshold, social cooperation breaks down. The societal order collapses. On the way to this collapse we can always observe the same phenomena.

One of these phenomena is something we have often discussed in these pages: money is not 'neutral'. When additional money is introduced into the economy, whether by means of a credit expansion that creates additional fiduciary media (deposit money ex nihilo) or outright inflation on the part of the government by printing of currency or discounting government debt with the central bank, there are always winners and losers.

Obviously it cannot be the case that society as a whole gets something 'for free' when new money enters the economy. Someone - namely those who are closest to the source - will gain at the expense of someone else - those who are further away from the source. This is why in the course of a progressing monetary inflation, we always observe that the rich become richer and the poor become poorer.

Distrust and Disorder

This month (and next month, and the one after that, and so forth ad infinitum) the Federal Reserve intends to create an additional $40 billion in bank reserves by buying mortgage backed securities with money it creates from thin air. Not all of these bank reserves will necessarily leak out into the economy, but in theory they could actually be levered up by the fractionally reserved banking system to a multiple of the original amount expended by the Fed.

This money will be created and enter the economy without anyone producing an offsetting contribution to the economy's pool of real funding. Obviously those with first dibs on the newly created money will be at a very big advantage: prices will only adjust over time, as the money percolates through the economy. The early receivers will still pay the old prices for goods and services - by the time lowly wage earners get paid their salaries, the effect on prices may already be noticeable. The more time passes, the more obvious this will become. People will notice that something is amiss, but most will be unable to diagnose the cause. Why does the paycheck no longer stretch as far as it once used to?

Those dependent on fixed incomes or their accumulated savings - the proverbial 'widows and orphans' - will be hit the hardest. The gap between rich and poor will widen ever more. It should be obvious that the rich have a far better chance to be among the winners of inflationary policy - as a rule the bulk of their wealth is in assets that rise in price disproportionately as inflation progresses.

It is generally no problem when the rich get richer - but it becomes one when the poor become poorer at the same time.

Distrust of the existing order begins to grow. Something must be done, but what? Many believe that the solution lies in even more intervention by the State. They begin to cry for a forcible redistribution of wealth. Politics becomes more polarized - political radicals and extremists come to the fore.

At the same time, the unseen, but actually most pernicious effects of the inflationary policy, continue to undermine the economy's structural integrity day after day. Capital malinvestment and capital consumption become an ever greater burden, gnawing away at the economy's ability to create wealth.

One could also say: the bills must be paid, but the means to pay them are slowly but surely eroded ever more.

At the very extreme end of an unending policy of monetary debasement stands the complete collapse of the existing societal order. As Grice shows in the historical examples he uses to buttress his points, this was of course never the intention of those pursuing the policy. They all thought they were only 'temporarily' helping the economy to get out of a tough spot. Often they were people who were well aware of the dangers, but still thought they could keep things under control. In short, they held that they could get whatever 'good' short term effects they expected the policy to produce without having to pay a price. They would step on the brakes in time: 'we'll do it just this once'.

Readers of this site may recall that we have pointed out again and again that this never works in practice. Once one embarks on a deliberate policy of monetary debasement, it becomes extremely difficult to 'step on the brakes' and discontinue the policy. This is because the temporary revival in bubble activities the policy produces tends to immediately die down again whenever the inflation as much as pauses. And so there is the constant temptation for policymakers to continue down the same path: 'we'll do it just one more time, that will surely do it'.

The Fed's Remaining Hawks

According to Ben Bernanke, it is all 'worth it', but is it really? In recent weeks we have heard from both the few remaining 'hawks' at the Federal Reserve as well as the many supporters and defenders of the newest iteration of 'QE'.

Let us briefly consider the 'hawks'. They are all presidents of Fed districts, i.e., not one of them is at the Fed's board of governors in Washington. This is so because in the districts, a banker or businessman is occasionally nominated to lead the district board. Only one third of the members of the district boards are nominated by the board of governors. As a result there are fewer pure academics presiding over the districts. The bankers and businessmen tend often to be against 'QE', as Richard Fisher of the Dallas Fed - one of the 'hawks' - recently pointed out in a speech he delivered to the Harvard Club of NYC. Fisher couldn't have made any clearer what he thinks of Bernanke's money printing antics:

"I felt an urge at the meeting last week to tie the chairman to the mast, Odyssean-style, and to stuff wax in the ears of my fellow committee members, in order to resist the Siren call of further large-scale asset purchases.

But I have no such powers. I am only one officer in the loyal crew that sails under the command of Admiral Bernanke. My reports were given a fair hearing. But neither they, nor the arguments of others who questioned the need to provide further accommodation, carried the day, and a decision was made."

We heard similar pronouncements from the two remaining 'hawks', Jeffrey Lacker and Charles Plosser. Apart from expressing concern about inflation and the danger to the Fed's credibility, Lacker and Plosser are both strongly opposed to the interference with credit allocation the MBS purchase program represents. They regard 'QE3' as straying into the realm of fiscal policy, which they believe the Fed should stay well clear of. Plosser e.g. said:

"I also opposed September's decision to purchase additional mortgage-backed securities. In general, central banks should refrain from preferential support for one sector or industry over another. Those types of credit-allocation decisions rightfully belong to the fiscal authorities, not the central bank. Engaging in such actions endangers our independence and the effectiveness of monetary policy."

As Bloomberg reports, Lacker holds a similar viewpoint:

""I strongly opposed purchasing additional agency mortgage- backed securities," Lacker said in a statement released yesterday by the Richmond Fed. "Such purchases, as compared to purchases of an equivalent amount of U.S. Treasury securities, distort investment allocations and raise interest rates for other borrowers."

Lacker said that "channeling the flow of credit to particular economic sectors is an inappropriate role for the Federal Reserve."

Lacker was the lone dissenter to the Federal Open Market Committee's Sept. 13 decision to purchase $40 billion a month in mortgage debt until the labor market improves and to hold interest rates near zero until at least mid-2015. Lacker has dissented from every FOMC decision this year."

(emphasis added)

{kind=link}

He even looks like a hawk: Richmond Fed president Jeffrey Lacker

(Photo by Andrew Harrer/Bloomberg)

One of the regional presidents formerly held to be among the 'hawks' has deserted them: Nayarana Kocherlakota has changed his tune. Formerly Kocherlakota opined that high unemployment was tied to a mismatch between the types of labor demanded and the types of labor offered, which no doubt contains more than a kernel of truth - although labor is generally regarded as a non-specific factor of production, the fact remains that it is not a monolithic aggregate. It should be obvious that after the bursting of the real estate bubble there are many people out there with skill sets that are no longer in demand, and it will take time for the adjustment to be made.

Somehow though, Kocherlakota has now become convinced that the Fed should continue pumping 'until the unemployment rate falls to 5.5%'. Not a word was breathed anymore about the 'mismatch' issue.

We haven't yet had a chance to take a closer look at Thomas Hoenig's successor at the Kansas Fed, Mrs. Esther George. We suspect however from a quick perusal of a recent speech of hers that her views are very much aligned with Thomas Hoenig's. Similar to Hoenig, she is very concerned with the risks posed by the 'too big to fail' banking institutions. So while the hawks may have lost the support of one Fed president, they may be gaining that of another.

However, the hawks are obviously not in chairman Bernanke's camp, in which we find the full complement of the ivory tower faction - the 'preemptive easing squad' that consists solely of academics who never had to run a business. All of them regard the economy as a machine: if only they pull the right levers, the machine will obey and produce the desired results. And of course, nothing can possibly go wrong.

The Hubris of Policymakers

Charles Evans, the 'über-dove' from the Chicago Fed, this week noted in an interview with CNBC that he actually thinks 'QE3' doesn't go far enough.

"The Federal Reserve is doing all it can to prop up an underperforming economy and will keep at it until the jobless rate falls below 7 percent, Chicago Fed President Charles Evans told CNBC.

Not only did Evans defend the central bank's recent announcement that it would embark on a third round of quantitative easing, but he also said he would have preferred if the Fed had been even more aggressive.

Evans said the Fed should keep policy loose until the unemployment rate falls below 7 percent. The current rate of 8.1 percent is too high and showing that the economy has yet to achieve sustainable growth, he said.

"That tells me that more accommodation would be appropriate, especially if it's effective," Evans said during a "Squawk Box" interview. "By all the analyses I've seen, it will be effective and the inflation risks are not very large at the moment."

[…]

"There's scope for doing more. I would have been doing more for a longer period of time," Evans said. "The committee made the determination that we're a lot closer to something like unacceptable growth - stall speed - and it's time to do more."

(emphasis added)

Charles Evans, president of the Chicago Fed: we're not inflating enough yet.

(Photo via The Chicago Federal Reserve Bank)

"In the Blinder and Zandi study, the "fact" that real GDP responds positively to government spending is built right into the model. No matter what the data had been - no matter what raw "observations" Blinder and Zandi had plugged in - the model could not possibly have spit out the answer, "The Obama package destroyed 800,000 jobs." The model assumed that stimulus policies help the economy, and after its whirring the model concluded that - stimulus policies help the economy."

It is the same with the models Bernanke, Yellen, Evans and Rosengren et al. use to justify their support for more money printing - it is a basic assumption of all these models that money printing and the artificial lowering of interest rates help the economy.

It is also assumed as a matter of course that there can be 'no inflation' (i.e., a rise in the 'general price level') as long as there are 'idle resources'. This is why Evans and the other 'doves' are so unconcerned about this point. Apparently they have blotted out the experience of the 1970's.

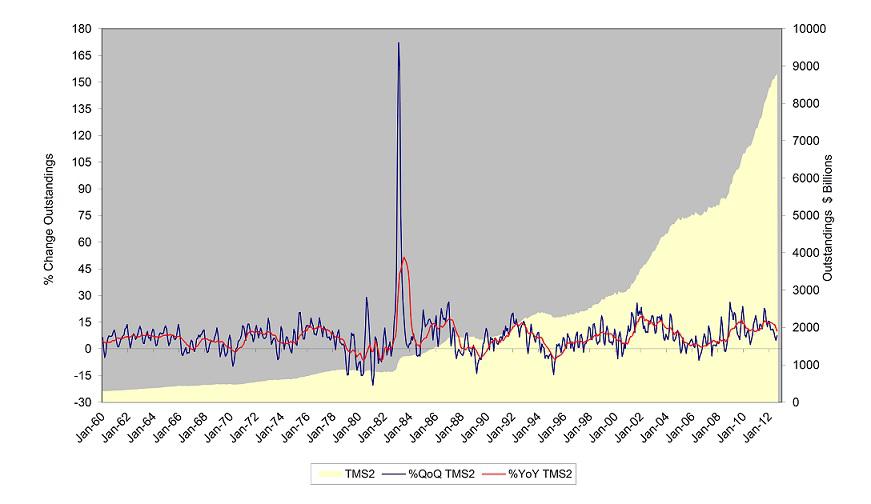

Moreover, as we often point out, if one defines inflation as an increase in the money supply, then we obviously have a huge 'inflation problem' already - as the true broad money supply TMS-2 has increased by over 80% since the beginning of 2008.

{kind=link}

The broad true US money supply TMS-2, via Michael Pollaro. No inflation problem?

This is in fact nicely demonstrated in the charts Dylan Grice included in his piece: all the historical episodes of inflationary crack-up booms have in common that the final phase - when the underlying monetary system breaks down - is marked by a massive acceleration in this loss of faith.

{kind=link}

An example from Grice's piece: the hyperinflation of the Weimar Republic. It took many years of inflationary monetary policy before the public's faith was suddenly lost and the monetary system broke down in a 'crack-up boom' in the space of less than two years.

"For controlling inflation, the key question is whether the Federal Reserve has the policy tools to tighten monetary conditions at the appropriate time so as to prevent the emergence of inflationary pressures down the road. I'm confident that we have the necessary tools to withdraw policy accommodation when needed, and that we can do so in a way that allows us to shrink our balance sheet in a deliberate and orderly way."

[…]

"Of course, having effective tools is one thing; using them in a timely way, neither too early nor too late, is another. Determining precisely the right time to "take away the punch bowl" is always a challenge for central bankers, but that is true whether they are using traditional or nontraditional policy tools. I can assure you that my colleagues and I will carefully consider how best to foster both of our mandated objectives, maximum employment and price stability, when the time comes to make these decisions."

In short, although it is impossible for a bunch of bureaucrats to know 'when precisely the right time' to 'take away the punchbowl' has arrived, we should still trust them that they will somehow know. Perhaps it is divine inspiration at work?

As to the famed 'exit' policy: there won't be an 'exit'. Recall that the 'exit' has been discussed many times over the past four years. But once you have an economy 'hooked' on a continuation of the inflationary policy, even a pause quickly puts paid to all the economic activities that depend on more and more inflation. Therefore, the 'right time' will never arrive. Should we actually come to the point where the Fed becomes confident enough to tighten policy somewhat, such as in 2004-2006, this will quickly produce the next crash. We will be back at square one then.

On the detrimental effects of the Fed's policies on savers, Bernanke had this to say:

"The concern about possible inflation is a concern about the future. One concern in the here and now is about the effect of low interest rates on savers and investors. My colleagues and I know that people who rely on investments that pay a fixed interest rate, such as certificates of deposit, are receiving very low returns, a situation that has involved significant hardship for some.

However, I would encourage you to remember that the current low levels of interest rates, while in the first instance a reflection of the Federal Reserve's monetary policy, are in a larger sense the result of the recent financial crisis, the worst shock to this nation's financial system since the 1930s. Interest rates are low throughout the developed world, except in countries experiencing fiscal crises, as central banks and other policymakers try to cope with continuing financial strains and weak economic conditions."

So, yes, we know we are waging a war on savers and depriving them of income in favor of bankers and speculators. But what can you do? It's crisis time! What remains unmentioned is that the crisis was the result of the same types of policies being implemented by the Fed after the bursting of the Nasdaq bubble. The assertion that 'inflation' is a 'concern for the future' is a non-sequitur given the lag times involved. Bernanke further:

"The crisis and recession have led to very low interest rates, it is true, but these events have also destroyed jobs, hamstrung economic growth, and led to sharp declines in the values of many homes and businesses. What can be done to address all of these concerns simultaneously? The best and most comprehensive solution is to find ways to a stronger economy. Only a strong economy can create higher asset values and sustainably good returns for savers. And only a strong economy will allow people who need jobs to find them. Without a job, it is difficult to save for retirement or to buy a home or to pay for an education, irrespective of the current level of interest rates.

The way for the Fed to support a return to a strong economy is by maintaining monetary accommodation, which requires low interest rates for a time. If, in contrast, the Fed were to raise rates now, before the economic recovery is fully entrenched, house prices might resume declines, the values of businesses large and small would drop, and, critically, unemployment would likely start to rise again. Such outcomes would ultimately not be good for savers or anyone else."

It is true that a tighter monetary policy would lead to another round of liquidation of malinvested capital and would therefore produce weakness in the 'economic data' in the short term. This is precisely why we say that there won't ever be an 'exit'. However, as we have already pointed out on previous occasions: the same things were said in 2000-2006. The narrative then went 'see, we told you it was necessary to engage in monetary pumping to rescue the economy. Look at the great success!'.

After all, the 'economic data' all began to look better while the housing bubble raged. Share prices and home prices rose, unemployment went down, everybody was happy. So why does the good chairman not consider that all of this was revealed as nothing but 'phantom prosperity' a short while later, bringing on the very crisis he now tries to 'inflate away' again?

Might it not be time to reflect on the longer term effects of the policy instead of the short term effects everybody admittedly loves?

We know the answer already of course: Bernanke and his supporters at the Fed firmly believe they will always have things 'under control'. They firmly believe that any untoward developments can be easily thwarted by pulling this lever or flicking that switch (he even mentioned increasing the rate the Fed pays on excess reserves as an example). But didn't the 2008 crisis already prove that they do not have things under control?

Bernanke is famed (unjustly we believe) for being an avid study of economic history, especially the Great Depression. Apparently his deliberations do not extend to more recent history, or to the extent that they do, are marred by the same errors that mark his interpretation of the 'lessons' imparted by the depression era. Evidently he also neglects to consider that he is definitely not the first policymaker who thought he had everything under control.

There are actually no examples of a policy of monetary debasement ever having produced a 'success'. This should not be too surprising: if one could simply print one's way to prosperity, everybody would do it. If the printing presses could do away with scarcity, we'd all be living in the Land of Cockaigne.

So in short, Bernanke and the other supporters of 'QE' at the Fed believe that they will be able to achieve what no-one has achieved before: to create a more wealthy and prosperous society by printing money.

Good luck with that idea.

{kind=link}

Fed chairman Ben Bernanke: What are you worrying about? We have everything under control.

No comments:

Post a Comment